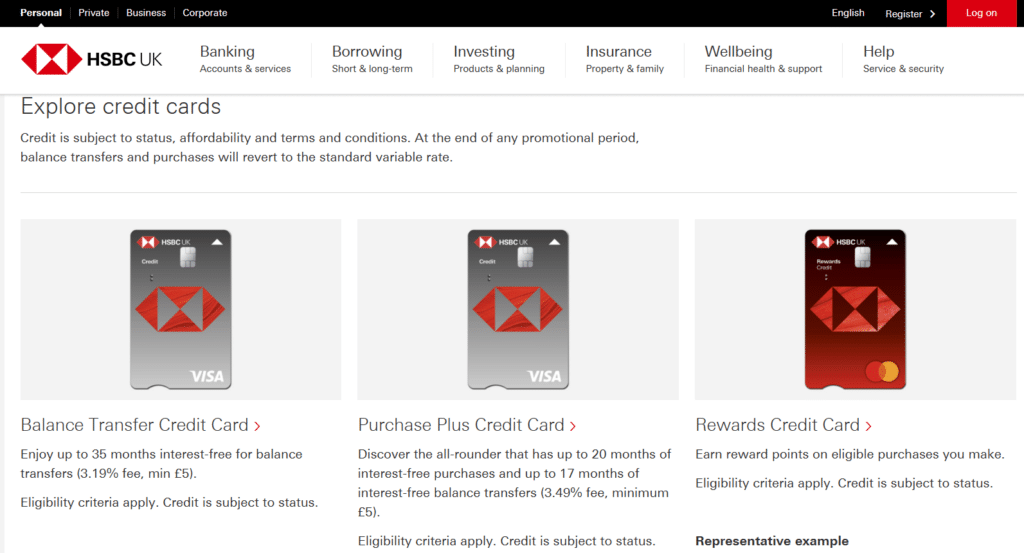

If you’re living in the UK and juggling credit card balances that never seem to shrink (because interest keeps eating your payments), a Balance Transfer Credit Card with up to 35 months interest-free can be a genuinely useful reset button. This type of card is built for one job: help you move existing credit card debt onto a new card and pay it down with less pressure, as long as you follow the rules of the offer.

This guide focuses on the practical side: exactly how to get the card, what to prepare before you apply, what happens after approval, and how to make sure you actually get the “up to 35 months interest-free” benefit.

Anúncios

Key offer recap (as provided):

- Up to 35 months interest-free on balance transfers

- Balance transfers must be completed within the first 60 days to qualify for the promotional period

- Balance transfer fee: 3.19% per transfer (minimum £5)

- Representative 24.9% APR (variable)

- Credit is subject to status, affordability, and terms & conditions

- The rate and promotional period offered depend on the lender’s assessment of your circumstances

What This Card Is (and Who It’s For)

This is a balance transfer-focused credit card. The main idea is to give you breathing room by letting you move balances from other credit cards and then pay 0% interest for up to 35 months on those transferred amounts.

This tends to suit people who:

- Already have credit card debt at high interest rates

- Want a single monthly repayment instead of multiple bills

- Need time (nearly three years, potentially) to clear a balance without interest piling on

It’s usually not ideal for people who want rewards, cashback, or travel points. The value here is the long 0% promotional window for debt repayment, not perks.

Balance Transfer Credit Card

Step-by-Step: How to Acquire the Card in the UK

Step 1: Get Clear on Your Goal (and Your Numbers)

Before you apply, do a quick “debt snapshot”. You want to know:

- How many credit cards you currently owe money on

- The balance on each card

- The interest rate you’re paying (approximate is fine)

- Your minimum monthly payments

- Your target monthly payment if interest was paused

This matters because balance transfer cards work best when you have a repayment plan. The 0% period is a tool — but your payments are what actually remove the debt.

A simple approach:

- Add up the balances you want to transfer

- Divide that total by 35 months (or fewer, to give yourself a cushion)

- That gives you a rough monthly payment target

Even if you don’t get the full 35 months, having a plan makes the offer far more useful.

Step 2: Check Your Eligibility Mindset (Without Guessing)

In the UK, credit card approval isn’t just “credit score good/bad”. The lender will look at affordability and your overall credit profile, which often includes:

- Income and employment status

- Existing credit commitments (loans, overdrafts, other cards)

- Recent applications for credit

- Payment history and utilisation

Important note from the offer: the promotional period is “up to” 35 months because the lender may offer a shorter period depending on their assessment.

What to do here:

- If you’ve applied for several credit products recently, consider pausing (multiple recent applications can hurt acceptance odds).

- If possible, reduce utilisation on existing cards a bit before applying.

Step 3: Gather What You’ll Need for the Application

Most UK credit card applications require similar information. Having it ready speeds things up and reduces mistakes:

- Full name, date of birth, UK address history (often 3 years)

- Employment details and income

- Bank details (sometimes)

- Monthly housing costs (rent/mortgage)

- Existing credit commitments (approximate monthly payments)

Tip: Be consistent with addresses and details. Even small mismatches (like abbreviated addresses) can trigger extra checks.

Step 4: Read the Key Documents (Yes, Actually)

This is the step people skip — and then regret.

Before you apply, read the important bits, especially:

- How the 0% balance transfer works

- The 60-day window for completing transfers

- The 3.19% fee (minimum £5) per transfer

- What happens if you miss a payment

- Whether purchases are charged interest (many balance transfer cards aren’t great for spending)

This offer explicitly says: “Please read the important documents before applying.” It’s not just legal fluff — it’s where the rules live.

Step 5: Apply for the Card

Once you apply, the lender will run a full assessment. Outcomes usually fall into one of these categories:

- Accepted (with a credit limit and promotional offer details)

- Referred (they need more checks)

- Declined

If accepted, you’ll be given:

- Your credit limit

- Your balance transfer terms (including whether you got the maximum promotional period)

Keep an eye on emails/letters or your online account area for the final confirmed details.

Step 6: Once Approved, Act Quickly — You Have 60 Days

This is the most important step in the entire process.

To qualify for up to 35 months interest-free, you must complete the balance transfers within the first 60 days of opening the account.

What to do immediately after receiving the card / account access:

- Log into your new credit card account (app or online banking)

- Find the “Balance Transfer” section

- Add the card(s) you want to transfer from:

- Provider name

- Card number (or relevant details requested)

- Amount to transfer

- Confirm the transfer(s)

Remember the cost:

- 3.19% fee per transfer (min £5)

Example:

- Transfer £2,000 → fee £63.80

- Transfer £100 → fee still £5

Plan your transfers strategically. If you’re transferring small amounts, the minimum fee can make it less efficient.

Step 7: Don’t Cancel Your Old Cards Too Quickly

A common mistake: transferring a balance and instantly closing the old card.

In many cases, it’s better to:

- Wait until the transfer completes (this can take several days)

- Check the old card balance is now £0

- Keep the old account open at least temporarily, unless you have a reason to close it (fees, temptation, poor terms)

Closing old accounts can affect your credit utilisation and average account age, which may impact your credit profile. There’s no one-size-fits-all here — just don’t rush.

Step 8: Set Up a Direct Debit for Minimum Payment (Non-Negotiable)

Even during a 0% period, you must pay at least the minimum payment each month. Missing payments can lead to:

- Loss of promotional rate

- Extra charges / interest

- Damage to your credit file

The simplest protection is setting up a direct debit for at least the minimum payment. Then you can choose to manually pay extra on top.

Step 9: Create a Repayment Strategy That Fits UK Reality

The magic of a 0% period is that your payment actually reduces the balance instead of fighting interest.

Two repayment strategies that work well:

Option A: Fixed monthly payment

- Take your balance (including transfer fees) and divide by the number of months you have

- Pay that every month

- Result: you finish around the end of the promotional period

Option B: Aggressive early payments

- Pay more in the first 6–12 months

- Then reduce payments later if needed

- This gives you flexibility if expenses rise

Either way, the goal is simple: clear the debt before the promo ends, so you don’t get hit by the standard variable rate (representative 24.9% APR variable).

What Makes This Card Attractive (Quick Summary)

This card is appealing mainly because:

- Up to 35 months is a long runway in the UK balance transfer market

- It helps you consolidate multiple balances into one payment

- It can reduce total cost of borrowing by avoiding interest during the promo period

The key conditions to respect are:

- Transfers within 60 days

- Fee of 3.19% (min £5) per transfer

- Keep up with monthly payments

HSBC Bank

Final Notes and Important Reminder

This product is subject to:

- Status

- Affordability

- Terms and conditions

And crucially:

- The rate and promotional period you receive depend on the lender’s assessment of your circumstances.

So while the offer is “up to 35 months”, you should apply expecting that your individual offer may vary — and you’ll only know for sure once approved.

If your primary goal is to reduce existing credit card debt with minimal interest pressure, this type of balance transfer card can be a smart, practical move — as long as you follow the steps above and treat the 60-day transfer window as a deadline.

Conteúdo criado com auxílio de Inteligência Artificial