If you’re in the United States and thinking about a travel-focused credit card, this guide walks you through Chase Sapphire – Step-by-step guide to apply. You’ll learn how to apply for Chase Sapphire, the Chase Sapphire application steps, and what to expect whether you choose the Chase Sapphire Preferred or Reserve.

This short introduction sets clear expectations: we cover eligibility and credit requirements, preparing documents, completing the online or in-branch application, improving approval odds, meeting welcome-bonus spending, and post-approval setup. The goal is practical — to help you apply for Chase Sapphire Card with fewer surprises and faster access to bonus points.

Anúncios

Chase Sapphire Preferred

Read on for a friendly, actionable walkthrough that focuses on real outcomes: better approval odds, quicker bonus qualification, and smarter use of Chase Ultimate Rewards. Whether you’re a frequent traveler or a casual diner, these steps make the Chase Sapphire US application process easier and more predictable.

Key Takeaways

- This guide explains how to apply for Chase Sapphire and the main Chase Sapphire application steps.

- You’ll learn eligibility requirements and how credit score ranges affect approval odds.

- Practical tips help you prepare documents and complete an online or in-branch application.

- Strategies cover timing, meeting welcome-bonus spend, and setting up rewards post-approval.

- Focus is on clear, actionable steps to apply for Chase Sapphire Card in the Chase Sapphire US program.

How to Apply for the Chase Sapphire Preferred® Credit Card in the U.S.: A Complete Step-by-Step Guide

The Chase Sapphire Preferred® is one of the most popular travel rewards credit cards in the United States, ideal for those who frequently spend on dining, travel, and everyday purchases. This guide walks you through each step of the application process, helping you apply quickly and securely.

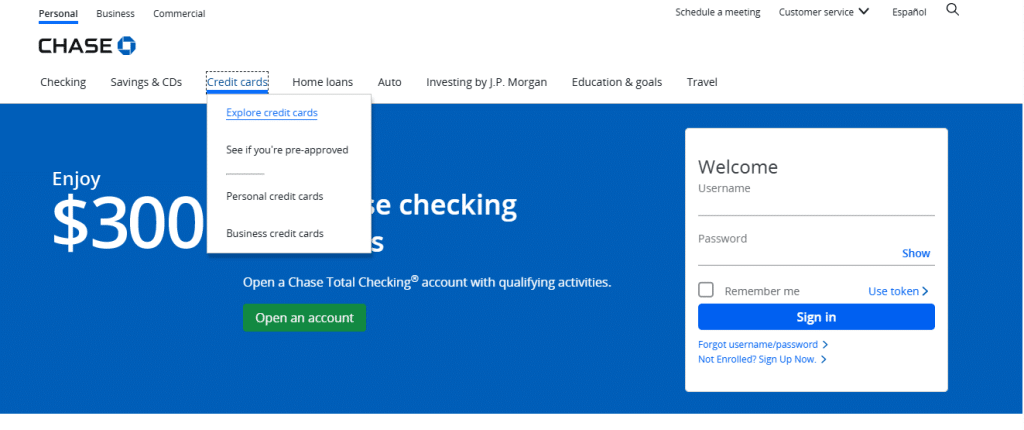

1 – Visit the Official Chase Website

Start by visiting www.chase.com.

From the top navigation bar, select “Credit Cards” and then click on “Explore Credit Cards.”

You’ll be taken to the section displaying all available Chase credit cards.

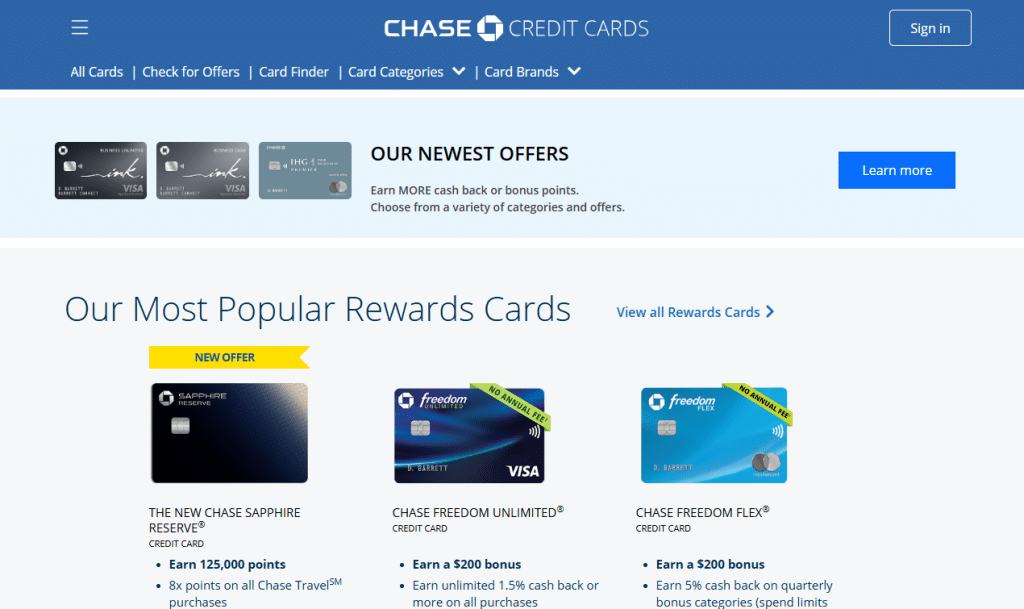

2 – Review Available Chase Cards

On the credit cards page, you’ll see several options, such as:

- Chase Freedom Flex®

- Chase Sapphire Reserve®

- Chase Sapphire Preferred®

- IHG One Rewards Premier

- UnitedSM Explorer Card

Each card caters to different needs, so take a moment to compare benefits and fees before choosing.

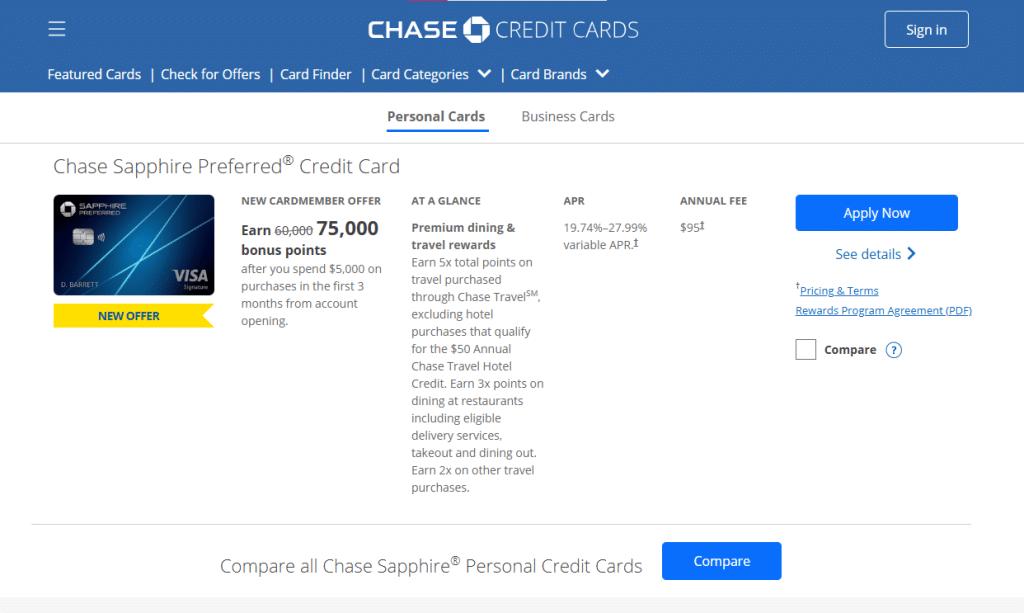

3 – Select the Chase Sapphire Preferred® Card

Locate the Chase Sapphire Preferred® — usually listed near the top of the page.

Click the “Apply Now” button to begin your application.

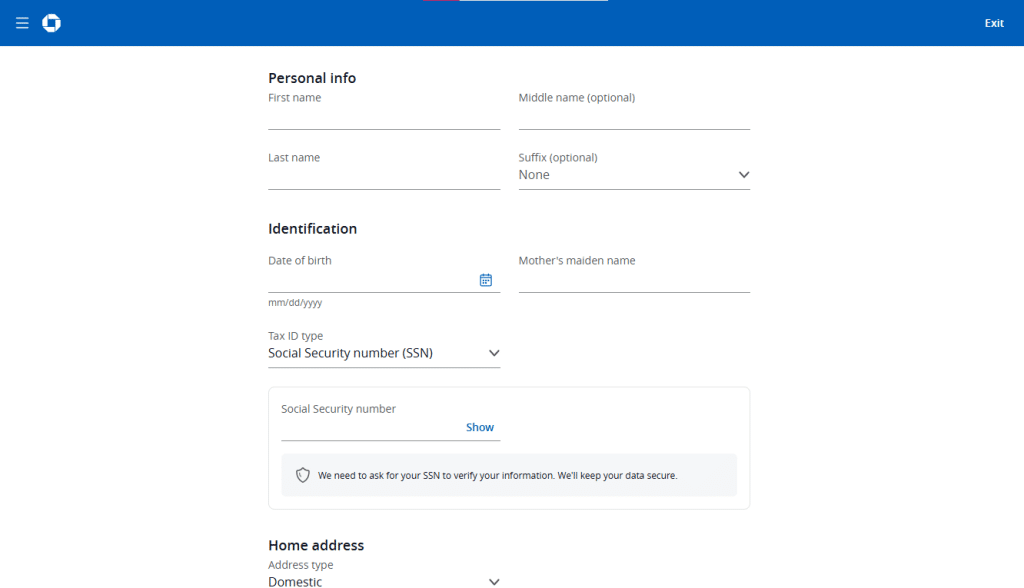

4 – Fill Out the Application Form

You’ll be directed to a secure application form. Provide the required details, including:

- Personal Information: Full name and date of birth

- Identification: Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN)

- Address: Residential and mailing address

- Contact Details: Phone number and email address

- Financial Information: Annual income and employment details

Once the form is complete, review all information carefully and submit your application. Chase will then perform a credit check to evaluate your eligibility.

If approved, your Chase Sapphire Preferred® card will arrive by mail within approximately 7–10 business days.

Main Benefits of the Chase Sapphire Preferred®

- Welcome Offer: Earn 60,000 bonus points after spending $4,000 in the first 3 months.

- Rewards: Earn 2X points on travel and dining and 1X point on all other purchases.

- Flexible Redemptions: Transfer points to major airline and hotel loyalty programs.

- No Foreign Transaction Fees: Ideal for international travelers.

- Comprehensive Travel Coverage: Includes trip cancellation insurance, baggage protection, and emergency assistance.

Basic Eligibility Requirements

Before applying, ensure you meet the following criteria:

- Residency: Must have a valid U.S. residential address.

- Age: Applicants must be at least 18 years old.

- Credit Standing: A good to excellent credit score (typically 700+) is recommended.

- Income: Steady and verifiable income source.

Approval and Card Delivery

After submitting your application:

- Approval: You may receive an instant decision or be notified later if additional verification is needed.

- Delivery: Approved applicants typically receive their card within 7–10 business days.

Once received, activate your card through Chase Online Banking, the mobile app, or by phone.

About Chase Bank

Chase Bank (JPMorgan Chase Bank, N.A.) is one of the largest and most trusted financial institutions in the United States. It provides a wide range of financial products and services, including checking and savings accounts, loans, investments, and credit cards.

History and Reputation

Chase is part of JPMorgan Chase & Co., founded in 1799, and operates across all 50 U.S. states and in over 100 countries worldwide.

Chase bank

Global Ranking and Stability

It is consistently ranked among the top global banks in total assets and customer trust, known for its strong financial stability, security, and commitment to customer service.

Final Thoughts

Applying for the Chase Sapphire Preferred® is a straightforward process that can be completed entirely online.

Simply visit the Chase website, select the card, fill out the form, and submit your application.

Once approved, you’ll be ready to enjoy valuable travel rewards, flexible redemption options, and premium benefits — all designed to make your financial and travel experiences more rewarding.

Overview of Chase Sapphire cards and benefits

The Chase Sapphire family offers clear choices for travelers and diners. Cardholders get elevated points on restaurants and travel, transfer options to major airline and hotel partners, and protections that ease trip hiccups. Comparing features helps match a card to real habits and budgets.

Differences between Chase Sapphire Preferred and Reserve

Preferred vs Reserve differences show up in fees, earning rates, and perks. Preferred carries a lower annual fee and a strong return on casual travel and dining spend. Reserve charges a higher annual fee but adds premium benefits that may offset that cost for frequent travelers.

Reserve usually earns higher points on travel and dining and gives a bigger redemption boost through Chase Ultimate Rewards when booking travel. Preferred still lets you transfer points to partners like United, World of Hyatt, and British Airways.

Insurance and credits differ, too. Reserve often includes primary rental car insurance, a travel credit that offsets part of the annual fee, and Priority Pass lounge access. Preferred provides solid travel protections and purchase safeguards without the same suite of premium extras.

Key travel and dining rewards

Both cards reward restaurants and travel purchases, making them strong tools for foodies and travelers. Points earn faster on dining and many travel categories, then move to partners such as Southwest, Air France/KLM, Marriott Bonvoy, and IHG for high-value redemptions.

Beyond points, benefits include trip delay and cancellation coverage, purchase protection, and extended warranties. These protections vary by card level, so read the terms to know what applies in each case.

Annual fees, signup bonuses, and long-term value

Signup bonus offers tied to a minimum spend are a major draw. Offers change over time, so check current promotions before applying. Evaluate the signup bonus against the required spend and your normal monthly outlays.

Think about annual fee versus recurring value. A higher annual fee can be worth it if you use travel credits, lounge access, and the boosted redemption value that Reserve provides. Preferred often delivers better return for moderate travelers who prefer a lower annual fee and solid baseline rewards.

Before applying, review current Chase terms on chase.com to confirm the latest signup bonus and benefit details. That step ensures your choice aligns with expected use and long-term value.

Who should apply for a Chase Sapphire card

Chase Sapphire cards reward people who spend on travel and dining. If you travel several times a year for work or leisure and enjoy dining out, a frequent traveler card or dining rewards card can stretch your dollars through bonus points and transfer partners.

Ideal applicant profiles and spending habits

The ideal applicant Chase Sapphire is someone who charges travel, flights, rideshares, hotels, and restaurants to one primary card. Cardholders who meet the signup minimum spend without overspending gain the most from welcome bonuses and elevated category multipliers.

Business travelers and leisure travelers who value travel protections, like trip delay insurance and primary rental car coverage, will find the features useful. People who prefer flexible points for award travel or who use partners such as United, Southwest, Hyatt, or Marriott enjoy added value.

Credit score ranges and financial readiness

Most approvals favor applicants with good to excellent credit. A typical credit score for Chase Sapphire in successful applications is 700 or higher, though approvals can occur in the high 600s when income and existing Chase relationships help.

Financial readiness means stable income, low-to-moderate credit utilization, and few recent credit inquiries. Avoid applying after a bankruptcy or when balances are high. Responsible card usage requires paying balances in full to prevent interest charges that negate reward value.

Frequent travelers, foodies, and points maximizers

Frequent travelers get outsized value by booking through travel portals or transferring points to airline and hotel partners. Foodies benefit from a dining rewards card since many purchases earn bonus points at restaurants and takeout.

Points maximizers who combine Chase cards, track category bonuses, and move points to travel partners often achieve high redemption value. For those who rarely travel or cannot meet minimum spend responsibly, a cash-back or lower-fee card may be a smarter option.

Chase Sapphire – Step-by-step guide to apply

Preparing to apply makes the process quick and smoother. Gather your full legal name, Social Security number, date of birth, home address, email, and phone number. Add your employment status, employer name, total annual household income, and monthly housing payment or rent.

Keep documents nearby in case they are requested. Useful items include recent pay stubs, last year’s tax return, recent bank statements, and a utility bill for proof of address. If you have existing Chase accounts, note those details. Disclose any bankruptcy history or public records honestly.

To start online, go to chase.com and find the Chase Sapphire product page you want. Choose Preferred or Reserve and click Apply Now. Sign in to your Chase account if you have one, or continue as a new applicant. The in-branch process is straightforward: bring a valid photo ID, Social Security number, and proof of income or address. Ask a banker to submit your in-branch Chase application and they will guide you through the forms.

The online flow walks you through clear screens for personal information, income totals, and housing payment fields. You will review Chase’s terms and disclosures and then see an instant decision or a pending review notice. Some applicants receive instant approval, while others face manual underwriting or a quick phone call.

Follow a Chase application checklist to reduce delays. Be honest and consistent with income and employment. Report gross annual income and include household income when allowed. Enter exact mortgage or rent amounts when prompted about monthly housing payments.

Common prompts ask about citizenship, residency, and existing credit accounts. Answer factually on credit history and other cards. Mismatched address history or missing income details are common causes of delays. If any follow-up is needed, respond promptly to requests for documents or clarification.

If you prefer to apply online, remember to double-check entries before submission. To complete an in-branch Chase application, bring the same documents you would use online and speak with a banker if questions arise. These steps will help ensure a smoother review and faster decision.

Eligibility and credit requirements for Chase Sapphire

Applying for a Chase Sapphire card starts with understanding what Chase looks for in applicants. Clear credit habits, a stable income, and a tidy credit history raise approval odds. Check your standing before you apply to avoid surprises.

Minimum credit score guidelines

Chase does not publish a strict cutoff, yet approval trends favor applicants with good to excellent scores. A credit score Chase Sapphire applicants often aim for is 700 or higher. People with scores in the high 600s can sometimes be approved when other factors like low utilization and steady income are strong.

Chase’s 5/24 rule and how it affects approval odds

The Chase 5/24 rule is a widely observed internal policy. If you have opened five or more credit cards from any issuer in the past 24 months, you are likely to be declined for most Chase personal cards, including Sapphire. Business cards and older accounts sometimes fall into gray areas, yet exceptions are uncommon.

Other account and relationship considerations

Existing Chase relationships can help, but they do not guarantee approval. Holding checking, savings, or a mortgage with Chase may improve your profile in borderline cases. A history of delinquency, charge-offs, or recent hard inquiries can hurt approval chances.

Chase enforces rules on bonus eligibility and product history. You may not qualify for a new cardmember bonus if you have received one for the same product before. Pay attention to past Sapphire or Chase bonus receipts when assessing your odds.

Practical steps include reviewing your credit report for errors, counting recent card openings, and delaying an application if you are near the Chase 5/24 rule. Meeting Chase account requirements and managing your credit profile boosts the likelihood of a successful application.

How to optimize your application for approval

Timing matters when you apply for a Chase Sapphire card. Space out new accounts and avoid multiple hard inquiries in a short time. If you plan several cards, submit your Chase application first to help optimize Chase application outcomes and keep your 5/24 count lower.

Timing applications and managing recent inquiries

Check recent hard pulls on your credit report before you apply. If you opened cards in the past few months, wait until balances settle and inquiries age. Lowering credit utilization on major cards for a few billing cycles can boost your score and improve Chase approval odds.

Improving approval chances with household income reporting

When you complete the form, include lawful sources of income. This can include a spouse or partner’s earnings if you live together and share finances. Chase typically allows household income reporting when you qualify under their policy.

List recurring income such as salaries, bonuses, retirement pay, alimony, rental income, dividends, and investment distributions. Be accurate and keep documentation like pay stubs or recent bank statements ready. Clear reporting of household income Chase can make a meaningful difference in underwriting.

When to call reconsideration and what to say

If your application is declined or left pending, use the Chase reconsideration call number in the notice or the general reconsideration line. Stay calm and polite. Begin by confirming identity and the reason for the decision.

State your verified income sources, mention any existing Chase accounts and history, and correct any errors on the application such as address or SSN entry. Ask what specific information would change the decision and offer to provide verification documents if requested.

Prepare recent pay stubs, bank statements, or tax transcripts before you call. A concise, factual explanation often moves a pending decision. Good documentation and a clear summary of household income Chase can speed the process.

Small additional steps help. Pay down balances to lower utilization, close or freeze any new credit inquiries if feasible, and clear any minor public records. These moves tighten your profile and further improve Chase approval odds.

Understanding welcome bonuses and spending requirements

Welcome offers for Chase Sapphire cards usually follow a simple formula: earn the bonus after you spend a set amount, such as $4,000, within a fixed window from account opening. Verify current details on chase.com before you apply because offer amounts and timeframes change. Clear rules make it easier to plan how you will meet the bonus target.

How to qualify for bonus offers

Most offers require a single qualifying threshold of purchases in the first 90 days. Qualifying purchases for bonus typically include normal card transactions at merchants and online retailers. Transactions that do not count include cash advances, balance transfers, and purchases of money orders or traveler’s checks. Returns and disputes can reduce posted totals and slow progress.

Effective strategies to meet minimum spend fast

Time large planned expenses to fall inside the initial window. Home improvement bills, medical copays, and insurance premiums can push you to meet minimum spend quickly. Prepaying recurring bills where allowed and buying gift cards for stores you already use can help accelerate progress without changing spending habits.

Adding authorized users for family purchases is an option to consolidate spending. Authorized user charges generally post to the primary account and count toward the requirement. Use business expenses or tax-deductible purchases when appropriate, keeping careful records for accounting and taxes.

Steer clear of manufactured spending schemes that violate card terms. Those practices risk bonus denial and account closure. Always keep an eye on cash flow so you can pay balances in full and avoid interest that erodes reward value.

Tracking bonus progress and qualifying purchases

Use the Chase mobile app or online account to track posted transactions and see how close you are to the target. Track credit card bonus progress by maintaining a short checklist of big-ticket items and their expected posting dates. Note that some merchants, like hotels and airlines, may take longer to post.

Watch for pending transactions versus posted transactions; only posted charges count toward the bonus. If a merchant delays posting, call Chase customer service to confirm whether a charge will be counted. Regular monitoring reduces surprises and helps you meet minimum spend on schedule.

Card features to set up after approval

After your Chase Sapphire card arrives, take a few simple steps to lock in security and start earning. Quick setup saves time, prevents missed payments, and makes it easier to track rewards. Use the Chase mobile app or chase.com to complete most tasks within minutes.

Create or sign in to your Chase online account to activate your card. You can activate by phone or in the Chase app. Enroll in two-factor sign-in and set a secure password during Chase online setup to protect your account.

Link bank accounts for payments and set autopay. Choose to pay the statement balance or full balance to avoid interest charges. Turn on paperless statements so you get faster alerts and reduce clutter.

Enable account alerts for transactions and due dates. Set payment reminders, low-balance and high-spend notices, and travel notifications when you plan trips. Alerts help detect fraud early and keep spending within your budget.

To add family members, add authorized user Chase through your online profile or by calling customer service. Authorized users receive a card and can help you reach welcome bonus thresholds when issuer rules allow, but the primary cardholder remains responsible for charges.

Use spending controls when available to limit card use by authorized users. Monitor activity regularly and remove any user who misuses the card to protect your account and credit.

Enroll in Chase Ultimate Rewards and link airline or hotel loyalty programs. Set redemption preferences for transfers and statement credits so you maximize value from points and miles.

| Setup Task | How to Do It | Why It Matters |

|---|---|---|

| Activate card | Call Chase or use the Chase app to activate Chase card | Allows purchases and confirms receipt of the physical card |

| Chase online setup | Create account, enable two-factor sign-in, link Sapphire card | Secures access and centralizes statements and payments |

| Link accounts & autopay | Add bank account, choose autopay options, enable paperless | Prevents missed payments and avoids interest when set to full balance |

| Account alerts | Turn on transaction, due date, and travel notifications | Detects fraud early and helps manage budgets |

| Add authorized user Chase | Enroll online or by phone; set controls if offered | Shares card access, may speed bonus qualification, primary pays charges |

| Loyalty linking & rewards | Enroll in Ultimate Rewards, link frequent flyer and hotel accounts | Makes point transfers and redemptions more valuable |

Maximizing rewards with Chase Sapphire

Chase Sapphire cards earn flexible points that reward travel and dining. Use simple tactics to maximize Chase Sapphire rewards and keep options open for big redemptions. Small changes to where and how you spend can raise point value without extra cost.

Best categories for earning points

Dining and travel are the clearest winners on both the Preferred and Reserve. The Reserve pays a higher rate on travel booked through Chase and often adds bonus value on dining. The Preferred gives strong returns on restaurants and travel too.

Other bonus categories can include transit, streaming, and select groceries depending on current terms. Merchant category codes matter. Some merchants like ride-share apps or online travel agencies may code differently, which changes the points you earn. Check receipts and merchant descriptions when points seem off.

Using Chase Ultimate Rewards for travel and transfers

Redeem points through Chase Ultimate Rewards by booking in the portal or transferring 1:1 to airline and hotel partners. Transfer partners include United, Southwest, British Airways Avios, Air France/KLM Flying Blue, Iberia, Singapore KrisFlyer, World of Hyatt, Marriott Bonvoy, and IHG Rewards.

The Reserve often boosts portal redemptions with a multiplier that raises point value. For outsized value, transfer to partners and book business-class award flights or stay at Hyatt aspirational properties. Watch award space and compare portal pricing versus partner awards before moving points.

Combining points with other Chase cards for higher value

Pair Sapphire with no-annual-fee cards like Chase Freedom Flex or with Ink Business Preferred to combine strengths. Use Freedom Flex for rotating or non-bonus categories and Ink Business Preferred for high-value business spend. Then combine Chase points into your Sapphire account for travel redemptions.

Examples: earn 5x on quarterly rotations with Freedom Flex, move those points into Sapphire, and either book through the portal or transfer to Chase Ultimate Rewards transfer partners for premium flights. This lets you consolidate rewards and extract maximum value.

Practical strategies include monitoring partner award space, comparing portal price to transfer rates, and booking one-way segments across partners when needed. Preserve flexibility by holding points until a strong award appears, then move or redeem with confidence.

| Action | Best Card to Earn | Why It Helps | Example Outcome |

|---|---|---|---|

| Dining out | Chase Sapphire Reserve | Higher points on dining; strong portal value | Earn premium points, redeem for travel portal credit or transfer to airline |

| Quarterly rotating categories | Chase Freedom Flex | 5x on select categories that Sapphire lacks | Move points to Sapphire and redeem for award flights or Hyatt stays |

| Business spend | Ink Business Preferred | Large bonuses in common business categories | Consolidate into Sapphire for top travel redemptions |

| Booking through portal | Chase Sapphire Reserve | Redemption multiplier raises point value on portal bookings | Lower cash outlay for flights or hotels booked directly |

| Transferring to airline/hotel | Any Sapphire as transfer hub | 1:1 transfers unlock high-value award inventory | Business-class awards or Hyatt Category 7 stays for fewer points |

Fees, protections, and travel perks explained

Choosing between Chase Sapphire cards means weighing annual costs against real benefits. Chase Sapphire fees and perks vary by card, and a quick look at common features helps decide which fits your travel style.

Annual fee considerations

The Preferred card usually has a lower annual fee than the Reserve. The Reserve carries a higher fee but adds statement credits that can offset part of that cost. Count dining and travel rewards when calculating value. Use your typical spend and expected redemptions with Ultimate Rewards to estimate a break-even point.

Offset strategies include using any annual travel credit on the Reserve, maximizing bonus categories, and transferring points to partners for greater value. Run the math on whether perks like statement credits, enhanced redemption rates, and partner transfers cover the fee each year.

Travel insurance, purchase protections, and rental car coverage

Both cards offer a suite of protections, but coverage limits and terms differ. Typical protections include trip cancellation and interruption insurance, trip delay reimbursement, and baggage delay or loss benefits. Purchase protection and extended warranty coverage help with faulty or damaged items.

Rental car coverage is often a deciding factor. The Reserve commonly provides primary rental car coverage in the U.S., while the Preferred tends to offer secondary coverage. Review policy details before renting to understand deductible, exclusions, and whether you need to decline the rental agency’s collision coverage.

Before relying on these benefits, confirm current limits and procedures in Chase’s benefits guide. Filing a claim requires documentation and adherence to time windows set by Chase.

No foreign transaction fees and airport lounge access details

Both Sapphire cards typically waive foreign transaction fees, saving about 1%–3% on international purchases compared with cards that add a fee. That feature alone makes either card attractive for travelers.

Airport lounge access is a major perk that sets the Reserve apart. Priority Pass Chase Reserve membership is available after enrollment and grants access to participating lounges. Guest policies and enrollment requirements vary, so check the membership rules when planning travel.

| Feature | Chase Sapphire Preferred | Chase Sapphire Reserve |

|---|---|---|

| Typical annual fee | $95 | $550 |

| Statement credits | None | Annual travel credit (varies by offer) |

| Travel insurance Chase Sapphire | Trip delay, trip cancellation (limits apply) | Enhanced trip delay, trip cancellation, higher limits |

| Rental car coverage | Secondary rental car coverage | Primary rental car coverage in U.S. (subject to exclusions) |

| No foreign transaction fees | Yes | Yes |

| Airport lounge access | None | Priority Pass Chase Reserve membership available |

| Purchase protections | Limited purchase and warranty coverage | Broader purchase protections and higher limits |

Common application pitfalls and how to avoid them

Applying for a Chase Sapphire card can be smooth when you know the common traps. Small errors often trigger manual review or a denial. Read each question slowly and double-check entries before submitting.

Mistakes on the application that can delay approval

Typos in your name, Social Security number, or address are frequent Chase application mistakes. These simple slips force extra verification and slow down approval.

Inconsistent employment or income entries cause confusion. List current employer details exactly as on pay stubs or W-2s. If you recently opened other cards, failing to disclose them can prompt a manual review.

Misunderstanding income reporting and joint applicants

Income reporting Chase requires honest numbers. Report gross annual income you personally receive. You may include a partner’s income when you share finances and their earnings are available to pay the account.

Do not invent or inflate income to improve odds. Misrepresentation can lead to account closure or negative credit outcomes. Chase does not generally offer joint consumer accounts. For shared access, add an authorized user rather than seeking a joint-account structure.

Dealing with declined applications and next steps

If you get a declined Chase Sapphire notice, start by reading the reason provided. Check your credit reports for errors. A dispute can clear mistakes that caused the decline.

Call Chase’s reconsideration line to explain discrepancies or supply requested documents. Keep a log of call dates, reference numbers, and any files you send. This record helps track progress when you avoid credit card application errors in future attempts.

Consider waiting and addressing problem areas before reapplying. If 5/24 is the issue, pause new applications and review recent account openings. Apply for a lower-tier Chase card or a product from another issuer while you rebuild eligibility.

Quick checklist to reduce errors

- Verify name, SSN, and address match official documents.

- Use gross annual income and note household income only when appropriate.

- List current employment exactly as shown on pay records.

- Disclose recent credit card openings to avoid surprises during review.

- Keep a log of calls and documents if you need reconsideration.

| Issue | Impact | Quick Fix |

|---|---|---|

| Typos in personal info | Manual review or delay | Proofread against driver’s license and SSN card |

| Inconsistent income reporting | Possible denial or request for proof | Report gross income; include partner only if funds are shared |

| Undisclosed recent accounts | Triggers Chase scrutiny | List recent openings and wait if near 5/24 limit |

| Requesting joint account | Application mismatch; policy issue | Add authorized user instead of joint primary holder |

| Declined Chase Sapphire | Approval blocked | Review reason, check credit reports, call reconsideration |

Conclusion

This Chase Sapphire guide conclusion pulls everything together. We compared Sapphire Preferred and Reserve, outlined which applicants benefit most, and walked through collecting ID and income documents before you apply for Chase Sapphire. The article also explained Chase eligibility rules, including the 5/24 guideline, and provided tips to improve approval odds.

We covered welcome-bonus tactics, ways to meet minimum spend responsibly, and the best way to apply Chase Sapphire online or in-branch. Post-approval steps include activating your card, linking accounts, and setting up autopay. We also reviewed fee trade-offs, travel protections, and common application pitfalls with practical remedies.

Before you submit, follow this short checklist: confirm the current Chase offer, check your 5/24 status and credit score, gather proof of income and ID, plan how you’ll meet the minimum spend, and decide whether Preferred or Reserve fits your travel habits. If you decide to apply for Chase Sapphire, pay on time, keep utilization low, and redeem points strategically to maximize value.

Refer back to the relevant sections as you prepare, and verify current terms on chase.com before applying. Using this clear, step-by-step approach increases your chances of a smooth approval and long-term satisfaction with your card choice.

FAQ

What’s the main difference between the Chase Sapphire Preferred and Chase Sapphire Reserve?

What credit score do I need to have a good chance of approval?

How does Chase’s 5/24 rule affect my application?

What personal and financial information should I have ready before applying?

Can I include my partner’s income on the application?

How do I apply online versus in-branch?

What common application prompts might delay approval and how should I answer them?

What should I do if my application is denied or shows pending review?

How do sign-up bonuses work and what counts toward the minimum spend?

What are safe strategies to meet the minimum spending requirement quickly?

What should I set up right after approval?

Can I add authorized users and will their purchases count toward my bonus?

How do I maximize Chase Ultimate Rewards points?

Does the Reserve card give better redemption value than Preferred?

What travel protections and insurance do Sapphire cards offer?

Are there foreign transaction fees on Chase Sapphire cards?

How should I evaluate whether the annual fee is worth it?

What are the top mistakes applicants make that delay approval?

How can I improve approval odds before applying?

What is the best way to track my bonus progress and posted purchases?

If I’m denied due to 5/24, what are my next steps?

Are there limits on receiving the sign-up bonus if I’ve had a Sapphire card before?

Should I consider a different card if I rarely travel?

Where can I confirm the most current offers, benefits, and terms?

Conteúdo criado com auxílio de Inteligência Artificial