Anúncios

This article helps U.S. consumers navigate a clear, step-by-step path to Citi Double Cash approval. If you want to apply for Citi Double Cash, you’ll find practical guidance on preparing your credit profile, completing the application, and understanding what makes this cash back credit card approval straightforward.

The main selling point is simple: Citi Double Cash pays 2% back on purchases — 1% when you buy and 1% when you pay. That no-frills structure makes it an appealing everyday card for people who prefer steady cash back over rotating categories or complex bonuses.

Anúncios

Citi Double Cash

This guide is written for U.S.-based consumers with fair-to-good credit who seek a reliable cash back card. You do not need advanced credit knowledge to follow the steps here; the aim is to make the Citi Double Cash simple process easy to follow and to boost your odds of success when you apply for Citi Double Cash.

The article is organized to walk you from a quick overview and key benefits, through eligibility and credit prep, to the actual application process and what to expect afterward. We’ll finish with tips on maximizing value and when another card might suit you better.

Anúncios

Key Takeaways

- Citi Double Cash approval is often accessible for those with fair-to-good credit.

- The card offers a straightforward 2% cash back structure that’s easy to use.

- Prepare credit reports and reduce utilization before you apply for Citi Double Cash.

- Follow simple application steps to improve your chance of cash back credit card approval.

- Post-approval actions, like paying on time, help you get the most from the card.

Step-by-Step Guide: How to Apply for the Citi Double Cash® Credit Card

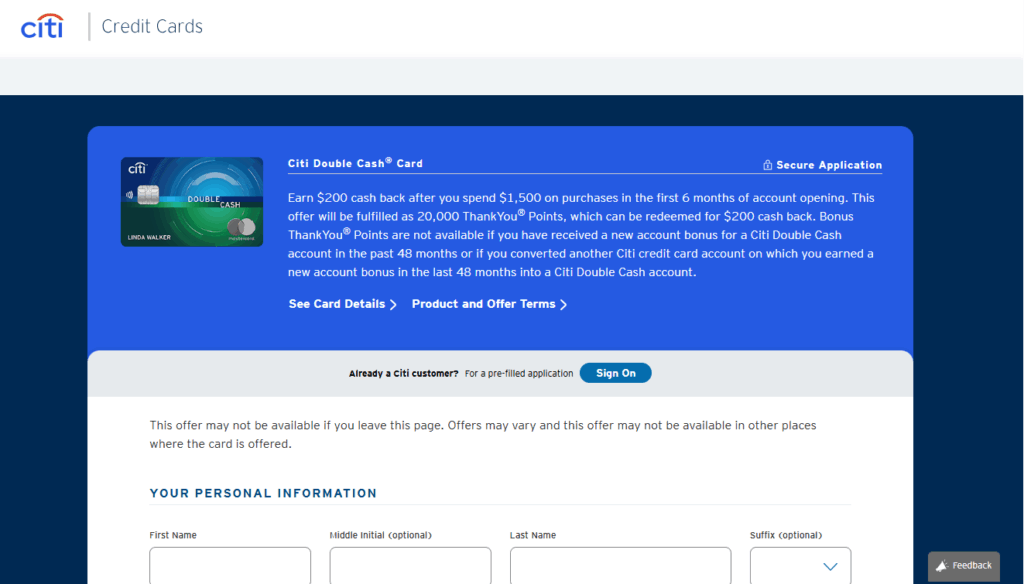

Applying for the Citi Double Cash® Card is a simple and secure process that can be completed online through the official Citi website. This comprehensive tutorial explains each step clearly, helping you apply efficiently and safely.

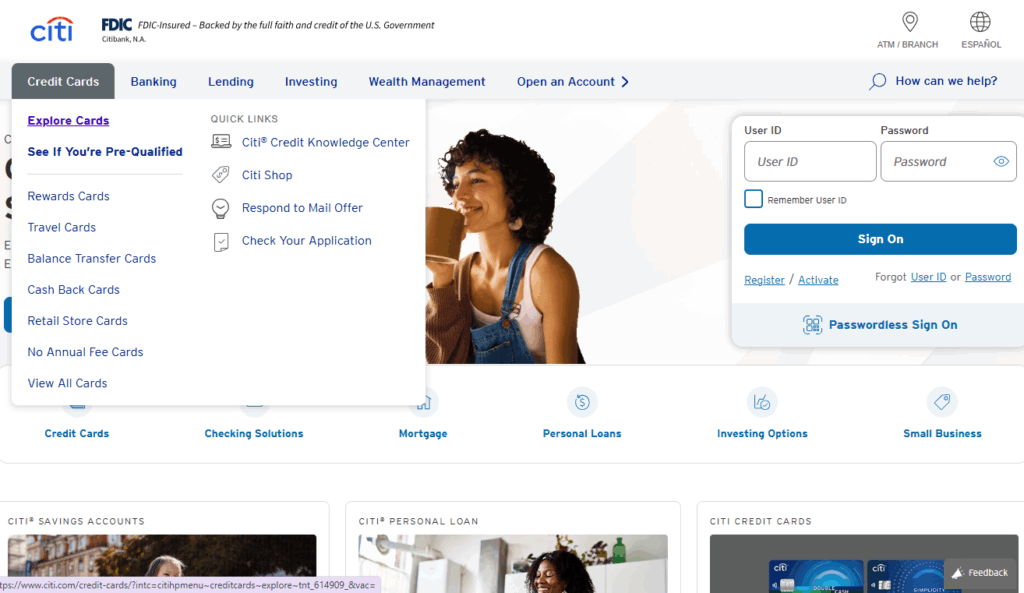

1 – Visit the Official Citi Website

Start by going to the official Citi homepage: https://www.citi.com/.

On the top navigation bar, click “Credit Cards” and then select “Explore Cards” to view all available credit card options.

2 – Explore the List of Citi Credit Cards

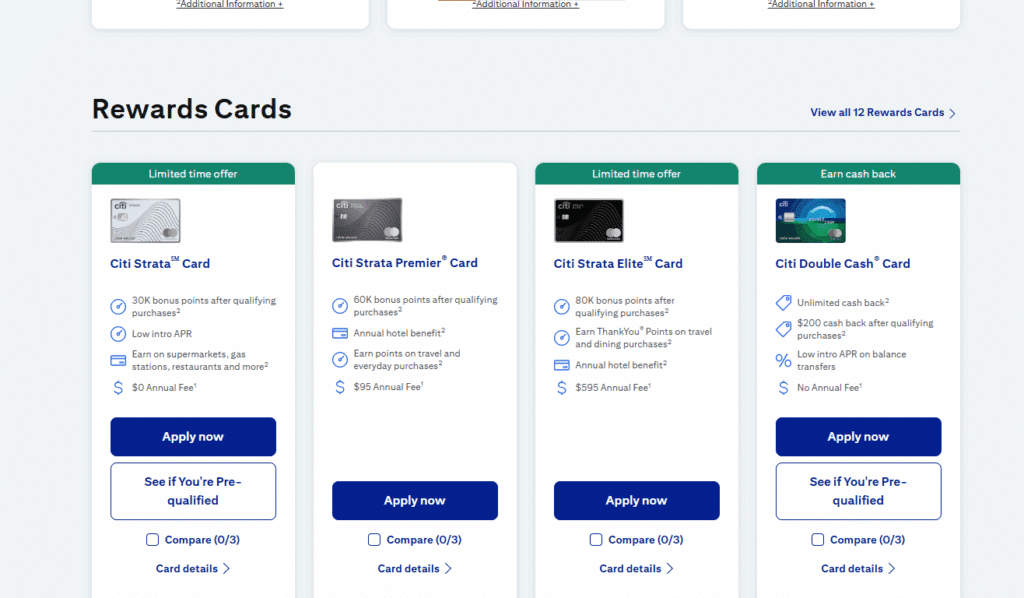

You’ll be directed to the credit card page, where Citi displays several card options, including:

- Citi® Diamond Preferred® Credit Card

- Citi® / AAdvantage® Platinum Select® World Elite Mastercard®

- American Airlines AAdvantage® MileUp® Card

- Costco Anywhere Visa® Card by Citi

You can refine your search using filters such as:

Balance Transfer, Travel, Rewards, No Annual Fee, Cash Back, and Retail.

Locate the Citi Double Cash® Card, usually found under the “Rewards Cards” section, and click the blue “Apply Now” button to begin.

3 – Fill Out the Application Form

After selecting “Apply Now,” you’ll be redirected to a secure online form. Enter the required details accurately, including:

- Full legal name

- Residential address

- Date of birth

- Phone number and email address

- Annual income and employment information

- Social Security Number (SSN)

Once completed, review your data to ensure it’s correct before submitting the form. After submission, Citi will process your application and provide a decision shortly.

4 – Official Application Page

You can also go directly to the card’s dedicated page:

https://www.citi.com/credit-cards/citi-double-cash-credit-card

This is the only official site for applications, guaranteeing that your information is protected throughout the process.

5 – Eligibility Requirements

Before you apply, make sure you meet the following basic criteria:

- Minimum Age: Must be at least 18 years old.

- Residency: Must have a U.S. residential address.

- Identification: A valid Social Security Number (SSN) is required.

- Credit History: A good credit score increases your approval chances, as the Citi Double Cash is typically aimed at users with strong credit profiles.

6 – Completing the Online Application Process

Step 1: Begin the Application

Click “Apply Now” on the official Citi Double Cash page to open the secure form.

Step 2: Enter Your Information

Provide accurate details, including your full name, address, date of birth, SSN, income, and employment status.

Step 3: Review and Submit

Before finalizing, double-check all entries for accuracy. Then click “Submit” to send your application for review.

7 – Approval and Card Delivery

Citi will review your information and perform a credit evaluation. Depending on your credit profile, you may receive an instant decision or a response within a few business days.

If approved, your Citi Double Cash® Credit Card will be mailed to your address within approximately 7–10 business days. You will receive activation instructions to start using your card immediately after receiving it.

8 – Final Notes

By applying for the Citi Double Cash® Credit Card, you’ll gain access to one of the most straightforward cashback programs available: 2% total cash back on every purchase — 1% when you buy and 1% when you pay.

Following this guide ensures a smooth, secure application process, letting you start enjoying the card’s consistent cashback and flexible benefits with complete confidence.

Overview of Citi Double Cash – Simple process to get approved

The Citi Double Cash card packs straightforward value for everyday spending. This short overview lays out the core Citi Double Cash features, what the card offers, why many U.S. consumers like it, and who should consider applying.

What the Citi Double Cash card offers

The main draw is a flat rewards rate: earn 1% when you buy and 1% when you pay, totaling 2% on most purchases. This 2% cash back card overview highlights a no annual fee design that keeps ongoing costs low for cardholders.

Basic protections include $0 fraud liability and purchase protection, with Citi customer service available for disputes. Redemption options normally include statement credit, direct deposit to eligible accounts, or a check, depending on current Citi choices.

Citi Bank

Why it’s a popular cash back card in the United States

Simplicity drives the card’s reputation. Many consumers prefer a flat-rate approach over rotating categories or enrollment. The 2% cash back card overview explains how uniform rewards make budgeting and rewards tracking easy.

No annual fee and broad reward coverage mean the card suits people who spend across many categories. That steady predictability keeps the Citi Double Cash features attractive for long-term use and pairing with specialty bonus cards.

Who should consider applying

Consider this card if you want consistent rewards without managing category calendars. The card fits users who pair a baseline cash back card with other cards that offer category bonuses.

People with fair-to-excellent credit who make regular monthly payments will see the most value. For readers wondering who should get Citi Double Cash, the right fit is a steady spender seeking low-cost, passive rewards.

Key benefits and rewards of Citi Double Cash

The Citi Double Cash card is prized for its clarity and steady returns. Cardholders earn a reliable flat rate that is easy to track and pairs well with bonus-category cards for more value.

How the 2% cash back works: earn and redeem

The mechanics are simple: you earn 1% cash back when you buy and a second 1% when you pay that purchase. Paying your statement balance triggers the extra 1% for each settled charge. If a purchase remains unpaid, the second 1% does not post until you pay it off.

There are no categories to track and no enrollment steps. The rate applies to eligible purchases where Visa is accepted, subject to card network rules. To redeem Citi Double Cash rewards, use Citi’s rewards portal to convert earnings into statement credits, checks, or other Citi-supported options. Check current thresholds and options inside your account before you redeem Citi Double Cash.

Additional perks and cardholder protections

Citi card protections include $0 liability for fraud on unauthorized transactions. The card can offer purchase protection and extended warranty coverage for qualifying items, with limits and terms set by Citi.

Cardholders get access to Citi customer support and online tools for account management. Some promotions, such as price-matching tools or limited-time offers, may appear from time to time; availability can vary and should be confirmed on Citi’s site.

Comparing rewards to competing cash back cards

In a cash back comparison, Citi Double Cash excels for steady return seekers. It lacks rotating bonus categories that can spike short-term earnings. Cards like Chase Freedom Flex give big returns in select categories, which can beat a flat rate if you max those categories.

Flat-rate rivals such as Wells Fargo Active Cash match the simplicity of Citi Double Cash. Differences show up in signup bonuses, travel protections, and APRs, so evaluate those elements based on your spending habits. Many users make Citi Double Cash a backbone card and pair it with a category bonus card to boost total returns.

| Feature | Citi Double Cash | Chase Freedom Flex | Wells Fargo Active Cash |

|---|---|---|---|

| Base rewards | 2% cash back (1% purchase + 1% pay) | 1% base; rotating 5% categories quarterly | 2% flat cash back |

| Enrollment for bonuses | No enrollment needed | Quarterly activation required | No enrollment needed |

| Signup bonus | Varies; check current offer | Often offers signup bonus | Often offers signup bonus |

| Consumer protections | Citi card protections: $0 fraud liability, purchase protection, extended warranty | Strong purchase and travel protections | Standard fraud protection and some purchase coverage |

| Best use case | Steady spenders who pay balances monthly and want simple rewards | Shoppers who can maximize rotating categories | Consumers seeking a flat-rate alternative with bonuses |

Eligibility criteria and credit requirements

Before applying for the Citi Double Cash card, review the basic rules that guide approval. Lenders look beyond a single number. They check payment history, available income, recent inquiries and account activity to form a complete picture of an applicant.

Typical credit score range for approval

Citi Double Cash eligibility tends to favor applicants with good to excellent credit. The credit score needed often falls in the mid-600s to the 700s and above. Applicants with scores below this band may still apply, but they face a higher chance of denial or lower credit limits.

Income and residency requirements for U.S. applicants

To qualify, you must be a U.S. resident and provide a valid Social Security number or ITIN. Citi asks for income details to confirm repayment ability. Acceptable income sources include wages, self-employment earnings, retirement payments and household income. No fixed minimum income is published, yet verifiable, steady income improves approval odds.

How existing Citi relationships can affect approval odds

Existing accounts with Citibank can help your application. A history of on-time payments, active checking or savings accounts and responsible card use may boost your chances. Citi approval factors also include recent Citi card openings, current utilization of Citi credit lines and recent credit inquiries. Too many recent approvals with Citi can trigger internal limits.

Use these points to assess your readiness and plan next steps. Update income records, check credit reports and consider account history with Citibank when preparing to apply.

Preparing your credit profile before applying

Before you apply, take a few focused steps to prepare credit for Citi Double Cash. A tidy credit profile raises your odds of approval and makes the card work better for you after approval. Start with a clear plan and small, consistent actions.

Checking your credit report and correcting errors

Pull your reports from Experian, Equifax, and TransUnion through AnnualCreditReport.com. Scan for incorrect accounts, wrong balances, or unfamiliar inquiries. Inconsistent personal details like name, address, or Social Security number can cause trouble; correct them so each bureau shows the same information.

If you spot inaccuracies, file disputes quickly. Provide supporting documents such as billing statements or identity verification. Track dispute outcomes and follow up until each error is resolved. Taking time to fix credit report errors reduces surprises during Citi’s review.

Strategies to improve your credit score quickly

Pay down high-interest balances first to improve credit fast. Even modest reductions can lower your utilization and reflect positively within one billing cycle. Bring late payments current and focus on settling the oldest delinquencies to limit damage to your score.

Consider becoming an authorized user on a well-managed card if you trust the primary account holder. This can add positive payment history without new inquiries. Avoid opening multiple new accounts before applying, since clustered hard pulls can hurt approval chances.

Managing credit utilization and recent inquiries

Aim to reduce credit utilization to under 30%, ideally between 10% and 20%. Lower utilization signals responsible borrowing and helps improve approval odds for Citi Double Cash. Request credit limit increases on accounts in good standing to lower utilization, but ask if the issuer will do a soft pull first.

Space out hard inquiries. Multiple hard pulls within 30 to 90 days can flag risk to card issuers. Plan your application timing so recent inquiries are minimized and your credit picture looks stable when you apply.

Application process and tips for approval

Starting a Citi Double Cash application is quick when you know the steps and what to prepare. This short guide walks you through the online process, lists the documents to have on hand, and points out common pitfalls so you can avoid denial.

Step-by-step online application walkthrough

Visit Citi.com/cards or a verified Citi landing page to find the Citi Double Cash card. Click the Apply button to begin.

Enter your personal details: full name, current address, Social Security number or ITIN, and date of birth. Add contact info for fast communication.

Provide employment status, annual income or household income, and monthly housing payment. Double-check numbers before moving on.

Read the terms and disclosures, including APR, fees, and rewards, then submit. Many applicants get an instant decision. If your review is pending, Citi will tell you the next steps.

What to have ready: documents and information

Keep your Social Security number or ITIN and government ID nearby. A driver’s license or other government-issued ID speeds verification.

Have proof of income available if requested. Pay stubs, W-2s, and recent tax returns are common documents for credit card application reviews.

List your current address history, monthly housing payment, and details of existing debts. Accurate numbers help Citi assess debt-to-income context.

Use up-to-date contact info for the fastest processing. Clear, truthful answers reduce follow-up requests and improve your odds when you apply online Citi Double Cash.

Common reasons applications are denied and how to avoid them

Low credit scores or negative marks such as recent collections or bankruptcy often lead to declines. Fix errors on your credit report and rebuild key accounts before you apply.

High credit utilization and several recent inquiries can trigger a denial. Pay down balances and space out new credit requests to improve approval chances.

Insufficient or unverifiable income is another common reason. Report income honestly and be ready to provide supporting documents to avoid denial.

Too many recent accounts or frequent Citi applications may limit approval odds. Wait between applications and review issuer-specific limits when planning a Citi Double Cash application.

| Stage | What to do | Why it helps |

|---|---|---|

| Before applying | Check credit report, lower utilization, gather pay stubs and ID | Reduces errors, proves income, improves credit score |

| During application | Enter accurate personal and income details, review disclosures | Faster processing, fewer verification requests, clearer decision |

| After submission | Provide requested documents promptly if Citi asks | Speeds final decision and helps avoid denial due to missing info |

| If denied | Request a reconsideration, check the denial reason, correct issues | Shows willingness to cooperate, guides next steps for approval |

What to expect after you apply

After you submit your Citi Double Cash application, you may see an instant approval or a prompt that the decision is pending. Many applicants get an instant approval at the time of submission. If the system needs more checks, your application can move to pending review Citi and the wait can last from a few days to several weeks.

Instant approval means the account is opened and you receive next steps right away. If your application is pending review Citi, Citi may ask for documentation or route the file for manual underwriting. Manual review often extends timelines for security and verification.

When Citi requests paperwork, respond quickly to speed up processing. You can provide additional info Citi via the secure upload portal, by fax, or by mail following their instructions. Common requests include proof of income, identity verification, or clarification of recent account activity.

Keep copies of everything you send. Note the date you provide additional info Citi so you can reference it during follow-up calls. That record helps if you need to check back about missing documents.

To check your Citi application status use the confirmation number from your submission. Log in to Citi online banking if you already bank with Citi to see messages about the application. Calling Citi credit card customer service with your application details works well when you want a real-time update.

If you prefer online tracking, the Citi site accepts your application reference and displays status updates. When calling, have your social security number and confirmation handy to speed verification. Clear, timely follow-up often shortens the pending review Citi window and moves you closer to an outcome.

Maximizing value after approval

Once your Citi Double Cash card arrives, small habits yield big returns. Use the card for everyday purchases, watch billing dates, and set simple rules so rewards add up without extra effort.

Best practices to earn the most cash back

Make the Citi Double Cash your go-to for general spending to capture the flat 2% on most purchases. Pair it with a category card for groceries, gas, or travel to boost overall yield.

Always pay at least the statement balance on time. The second 1% cash back posts only when purchases are paid, so prompt payment protects your take-home rewards and credit health.

Track large buys and split payments if needed so you don’t miss the posted-pay requirement. Use alerts or multiple payments each month to keep reported balances low and spending under control.

Redeeming cash back: statement credit, check, and other options

Open the Citi rewards center to review redemption choices. You can redeem Citi cash back as a statement credit, request a check, or choose direct deposit where supported.

Check minimums and processing times before you redeem Citi cash back. Statement credits reduce your balance immediately. Checks may take longer, so time redemptions for cash flow or tax planning.

Managing your account to maintain a healthy credit profile

Use Citi’s online tools to manage Citi account settings, enable autopay, and set alerts for due dates. On-time payments are the strongest factor for sustained credit health.

Keep utilization low by paying down balances before the statement closing date. Review monthly statements for unfamiliar charges and use Citi’s dispute process quickly when needed.

- Tip: Make multiple small payments each month to lower reported utilization.

- Tip: Link your account to Citi alerts to avoid missed payments and protect credit health.

Potential drawbacks and who might want a different card

Before you commit to a Citi Double Cash card, weigh its trade-offs against your spending habits and financial plans. The card’s flat-rate rewards are simple and steady, but simplicity can mean missed opportunities for some users.

Limitations of the Citi Double Cash program

The Citi Double Cash limitations include a lack of category bonuses. You won’t get elevated rewards for groceries, gas, or travel like you would with some specialty cards. That matters if most of your spending falls into those buckets.

Another limitation is the reliance on paying off purchases to earn the full 2% back. Carrying a balance brings Citi APR into play and interest can wipe out rewards quickly. The card also tends to offer fewer premium travel perks such as lounge access or travel credits.

Scenarios when another card could be a better fit

If you spend heavily in specific categories, a card that returns 3–6% in those areas will often beat flat-rate earnings. For frequent flyers who want airport lounges, travel insurance, or transfer partners, a travel rewards card is usually superior.

People who expect to carry a balance temporarily should look for cards with a 0% introductory offer or lower ongoing rates. Those cards can save more than the 2% flat rate if balance transfer rates and introductory APR deals are favorable.

How balance transfers, interest rates, and fees factor in

Compare balance transfer rates carefully. Citi sometimes runs promotions on other products, but Citi Double Cash itself rarely includes a lengthy 0% transfer offer. If you need to move balances, check current terms on cards that focus on transfers.

Watch the Citi APR on purchases and cash advances. Interest can erase cash back gains fast. The absence of an annual fee is helpful, yet foreign transaction fees and late fees may still apply, so confirm the fee schedule before international travel or if you might miss payments.

Conclusion

The Citi Double Cash summary is simple: a flat 2% cash back on every purchase with no annual fee. That steady structure makes the card a reliable choice for everyday spending and for people who prefer clear, predictable rewards instead of rotating categories or large sign-up bonuses.

To get approved Citi Double Cash, focus on your credit profile before you apply. Check your credit reports for errors, lower credit utilization, and report accurate income. Follow a careful application process and have documents ready to speed any verification steps.

Decide if is Citi Double Cash right for you by weighing steady rewards against trade-offs. If you want broad, uncomplicated cash back, this card fits well. If you seek high bonuses in specific categories, consider pairing Citi Double Cash with a category card to boost total rewards.

Next steps: review current terms on Citi.com, pull your credit reports, and prepare documentation before applying. These actions will improve approval odds and help you get the most value from the Citi Double Cash card.

FAQ

What is the Citi Double Cash card and why should I consider it?

Who is eligible to apply for the Citi Double Cash?

What credit score do I need to get approved?

What documents and information should I have ready before applying?

How does the 2% cash back actually work?

How can I redeem my Citi Double Cash rewards?

Will having other Citi accounts help my approval odds?

What are common reasons applications are denied and how can I avoid them?

How long does the application decision take?

If Citi asks for more information, how should I respond?

How can I boost my approval odds quickly if I plan to apply soon?

What are the main advantages and the key drawbacks of the Citi Double Cash?

What is the Citi Double Cash card and why should I consider it?

Who is eligible to apply for the Citi Double Cash?

What credit score do I need to get approved?

What documents and information should I have ready before applying?

How does the 2% cash back actually work?

How can I redeem my Citi Double Cash rewards?

Will having other Citi accounts help my approval odds?

What are common reasons applications are denied and how can I avoid them?

How long does the application decision take?

If Citi asks for more information, how should I respond?

How can I boost my approval odds quickly if I plan to apply soon?

What are the main advantages and the key drawbacks of the Citi Double Cash?

FAQ

What is the Citi Double Cash card and why should I consider it?

The Citi Double Cash is a no-annual-fee cashback card that pays a simple 2% on most purchases — 1% when you buy and 1% when you pay. It’s a good fit for U.S. consumers who want predictable rewards without tracking rotating categories, and it works well as a backbone card paired with bonus-category cards like Chase Freedom Flex or American Express Blue Cash for category-specific boosts.

Who is eligible to apply for the Citi Double Cash?

U.S. residents with a valid Social Security number or ITIN and a credit profile in the fair-to-excellent range are the target audience. Typical approvals favor applicants with FICO scores in the mid-600s and above, but Citi reviews income, account history, recent inquiries, and existing Citi relationships when making decisions.

What credit score do I need to get approved?

While Citi doesn’t publish a strict cutoff, approvals commonly occur for applicants with scores in the mid-600s to 700s and higher. Applicants with lower scores may still apply, but they face higher odds of denial or lower credit limits because Citi evaluates several factors beyond the numeric score.

What documents and information should I have ready before applying?

Have your Social Security number or ITIN, current address, date of birth, employment status, and annual income (or household income) ready. Keep proof of income such as recent pay stubs, W-2s, or tax returns available in case Citi requests verification. A government ID and details about monthly housing payments and existing debts will also speed up the process.

How does the 2% cash back actually work?

You earn 1% cash back at the time of purchase and an additional 1% when you pay that purchase. To trigger the second 1%, you must pay down the purchase (or your statement balance). Unpaid balances won’t earn the second 1% until they are paid, so paying on time maximizes rewards.

How can I redeem my Citi Double Cash rewards?

Rewards are redeemable through Citi’s rewards portal, typically as statement credits, direct deposits to eligible accounts, or checks. Redemption options and thresholds can change, so check Citi’s current rewards center for processing times and minimums before redeeming.

Will having other Citi accounts help my approval odds?

A positive history with Citi — such as on-time payments for bank or card accounts — can help. However, too many recent Citi openings or closings, or a cluster of recent Citi inquiries, can trigger internal limits and lower approval chances. Maintain good standing and space out new accounts when possible.

What are common reasons applications are denied and how can I avoid them?

Common denial reasons include low credit scores, high credit utilization, too many recent hard inquiries, insufficient or unverifiable income, and errors on the application. To reduce risk, check credit reports for errors, lower revolving balances (aim for under 30%, ideally 10–20%), verify income documentation, and double-check all application entries before submitting.

How long does the application decision take?

Many applicants receive an instant decision online. If additional review is needed, Citi may mark the application as pending and request documents; review times can range from a few days to several weeks depending on workload and whether manual underwriting is required.

If Citi asks for more information, how should I respond?

Provide requested documents promptly through Citi’s secure upload portal, fax, or mail following their instructions. Typical requests include proof of income, identity verification, or clarification of account history. Keep copies and note submission dates for follow-up calls.

How can I boost my approval odds quickly if I plan to apply soon?

Pay down high balances to lower utilization, bring past-due accounts current, avoid opening new accounts in the 30–90 days before applying, and ensure your income and personal information are consistent across credit reports. Requesting a credit limit increase on existing cards (with awareness of whether the issuer performs a hard pull) can also lower utilization.

What are the main advantages and the key drawbacks of the Citi Double Cash?

Advantages: a simple flat 2% cash back on most purchases, no annual fee, useful card protections like

FAQ

What is the Citi Double Cash card and why should I consider it?

The Citi Double Cash is a no-annual-fee cashback card that pays a simple 2% on most purchases — 1% when you buy and 1% when you pay. It’s a good fit for U.S. consumers who want predictable rewards without tracking rotating categories, and it works well as a backbone card paired with bonus-category cards like Chase Freedom Flex or American Express Blue Cash for category-specific boosts.

Who is eligible to apply for the Citi Double Cash?

U.S. residents with a valid Social Security number or ITIN and a credit profile in the fair-to-excellent range are the target audience. Typical approvals favor applicants with FICO scores in the mid-600s and above, but Citi reviews income, account history, recent inquiries, and existing Citi relationships when making decisions.

What credit score do I need to get approved?

While Citi doesn’t publish a strict cutoff, approvals commonly occur for applicants with scores in the mid-600s to 700s and higher. Applicants with lower scores may still apply, but they face higher odds of denial or lower credit limits because Citi evaluates several factors beyond the numeric score.

What documents and information should I have ready before applying?

Have your Social Security number or ITIN, current address, date of birth, employment status, and annual income (or household income) ready. Keep proof of income such as recent pay stubs, W-2s, or tax returns available in case Citi requests verification. A government ID and details about monthly housing payments and existing debts will also speed up the process.

How does the 2% cash back actually work?

You earn 1% cash back at the time of purchase and an additional 1% when you pay that purchase. To trigger the second 1%, you must pay down the purchase (or your statement balance). Unpaid balances won’t earn the second 1% until they are paid, so paying on time maximizes rewards.

How can I redeem my Citi Double Cash rewards?

Rewards are redeemable through Citi’s rewards portal, typically as statement credits, direct deposits to eligible accounts, or checks. Redemption options and thresholds can change, so check Citi’s current rewards center for processing times and minimums before redeeming.

Will having other Citi accounts help my approval odds?

A positive history with Citi — such as on-time payments for bank or card accounts — can help. However, too many recent Citi openings or closings, or a cluster of recent Citi inquiries, can trigger internal limits and lower approval chances. Maintain good standing and space out new accounts when possible.

What are common reasons applications are denied and how can I avoid them?

Common denial reasons include low credit scores, high credit utilization, too many recent hard inquiries, insufficient or unverifiable income, and errors on the application. To reduce risk, check credit reports for errors, lower revolving balances (aim for under 30%, ideally 10–20%), verify income documentation, and double-check all application entries before submitting.

How long does the application decision take?

Many applicants receive an instant decision online. If additional review is needed, Citi may mark the application as pending and request documents; review times can range from a few days to several weeks depending on workload and whether manual underwriting is required.

If Citi asks for more information, how should I respond?

Provide requested documents promptly through Citi’s secure upload portal, fax, or mail following their instructions. Typical requests include proof of income, identity verification, or clarification of account history. Keep copies and note submission dates for follow-up calls.

How can I boost my approval odds quickly if I plan to apply soon?

Pay down high balances to lower utilization, bring past-due accounts current, avoid opening new accounts in the 30–90 days before applying, and ensure your income and personal information are consistent across credit reports. Requesting a credit limit increase on existing cards (with awareness of whether the issuer performs a hard pull) can also lower utilization.

What are the main advantages and the key drawbacks of the Citi Double Cash?

Advantages: a simple flat 2% cash back on most purchases, no annual fee, useful card protections like $0 fraud liability and purchase protection, and easy pairing with category cards. Drawbacks: no elevated category bonuses, potential lack of a signup bonus at times, and the need to pay purchases to earn the full 2% — carrying a balance can reduce effective rewards because interest may outweigh cash back.

When might another card be a better choice?

If you spend heavily in specific categories such as groceries, gas, dining, or travel where other cards offer 3–6% back, a specialized card may yield higher returns. Frequent travelers who value perks like lounge access or transfer partners might prefer a travel rewards card. Also consider a 0% APR card if you plan to carry a balance temporarily.

How should I manage my Citi Double Cash account to protect my credit score?

Make on-time monthly payments, keep reported balances low by making multiple payments each month if needed, monitor statements for unauthorized charges, and enable alerts and autopay in Citi’s online portal. Regularly reviewing your credit reports from Experian, Equifax, and TransUnion helps catch errors that could harm approval odds for future products.

Can I pair the Citi Double Cash with other cards to maximize rewards?

Yes. Many cardholders use Citi Double Cash as a baseline for general spending and pair it with category-focused cards like Chase Freedom Flex, American Express Blue Cash Preferred, or a travel card to capture elevated returns on groceries, gas, dining, or travel. This “backbone plus specialty” strategy often increases overall rewards.

Does the Citi Double Cash offer balance transfer promotions or other intro APR features?

The Citi Double Cash itself may not always include a long 0% introductory APR or balance transfer promotion. Citi periodically runs offers across its product line, so check current terms on Citi.com when applying. If you need a balance transfer, consider a Citi card or another issuer that specifically advertises a 0% transfer offer.

How often should I check my credit reports before applying?

Pull your credit reports from Experian, Equifax, and TransUnion via AnnualCreditReport.com at least once before applying to confirm accuracy. If you spot issues, dispute them promptly and follow up. Checking reports multiple months before applying gives time to resolve disputes and improve scores.

When might another card be a better choice?

How should I manage my Citi Double Cash account to protect my credit score?

Can I pair the Citi Double Cash with other cards to maximize rewards?

Does the Citi Double Cash offer balance transfer promotions or other intro APR features?

How often should I check my credit reports before applying?

fraud liability and purchase protection, and easy pairing with category cards. Drawbacks: no elevated category bonuses, potential lack of a signup bonus at times, and the need to pay purchases to earn the full 2% — carrying a balance can reduce effective rewards because interest may outweigh cash back.

When might another card be a better choice?

If you spend heavily in specific categories such as groceries, gas, dining, or travel where other cards offer 3–6% back, a specialized card may yield higher returns. Frequent travelers who value perks like lounge access or transfer partners might prefer a travel rewards card. Also consider a 0% APR card if you plan to carry a balance temporarily.

How should I manage my Citi Double Cash account to protect my credit score?

Make on-time monthly payments, keep reported balances low by making multiple payments each month if needed, monitor statements for unauthorized charges, and enable alerts and autopay in Citi’s online portal. Regularly reviewing your credit reports from Experian, Equifax, and TransUnion helps catch errors that could harm approval odds for future products.

Can I pair the Citi Double Cash with other cards to maximize rewards?

Yes. Many cardholders use Citi Double Cash as a baseline for general spending and pair it with category-focused cards like Chase Freedom Flex, American Express Blue Cash Preferred, or a travel card to capture elevated returns on groceries, gas, dining, or travel. This “backbone plus specialty” strategy often increases overall rewards.

Does the Citi Double Cash offer balance transfer promotions or other intro APR features?

The Citi Double Cash itself may not always include a long 0% introductory APR or balance transfer promotion. Citi periodically runs offers across its product line, so check current terms on Citi.com when applying. If you need a balance transfer, consider a Citi card or another issuer that specifically advertises a 0% transfer offer.

How often should I check my credit reports before applying?

Pull your credit reports from Experian, Equifax, and TransUnion via AnnualCreditReport.com at least once before applying to confirm accuracy. If you spot issues, dispute them promptly and follow up. Checking reports multiple months before applying gives time to resolve disputes and improve scores.

Conteúdo criado com auxílio de Inteligência Artificial