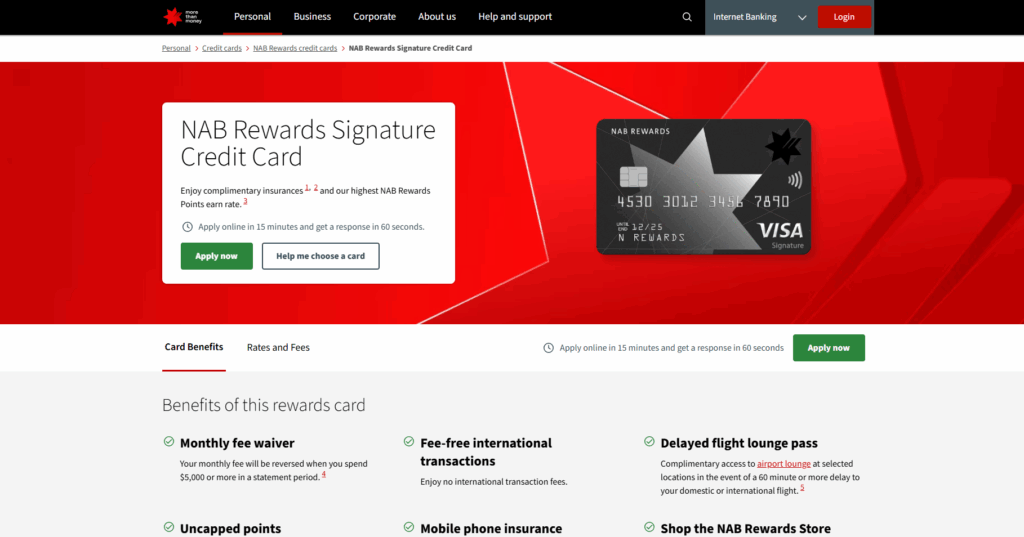

The NAB Rewards Signature card is perfect for Aussies wanting to earn points on daily buys. It covers who should think about getting the NAB Rewards card, what to expect when applying, and why it’s key to know about fees, welcome deals, and how to use points before applying.

If you live in Australia, are 18 or older, already with NAB or switching, this guide’s for you. It shows how to give the right info, avoid slips, and get the most points once your card is working.

Anúncios

Before going further, look at NAB’s latest product info online and check special deals. This makes sure you understand the current interest, costs and any point bonuses that make the card more valuable across Australia.

NAB Rewards Signature

Key Takeaways

- The NAB Rewards Signature card earns points on eligible buys and often has special welcome offers.

- People wanting the card need to be the right age and live in Australia.

- Get your documents ready and know what mistakes to avoid for a better chance at approval.

- Look at fees, interest rates and the product info on NAB’s site before deciding if it’s right for you.

- Buying certain things, using partner offers, and keeping an eye out for promotions can boost your points and their value.

NAB Rewards Signature Credit Card: A Friendly Guide to Applying and Understanding the Card

The NAB Rewards Signature Credit Card is a popular choice in Australia for people who want everyday flexibility and meaningful reward points while still managing costs. It’s especially suited for those who spend regularly on essentials and non-essentials alike, and who enjoy earning rewards that can be redeemed for travel, merchandise, gift cards, or frequent flyer programs.

One of the key attractions of this card is its rewards rate of 1.5 points for every $1 spent on eligible purchases. That makes it a strong option for cardholders who want a reliable way to accumulate points on everyday spending without getting tied into a narrow or complicated rewards scheme.

Below, you’ll find a step-by-step guide on how to apply for the NAB Rewards Signature Credit Card, an overview of its standout features, and a comparison with a well-known competitor — the American Express Velocity Credit Card.

What Makes the NAB Rewards Signature Credit Card Worth Considering?

Before we get into the application steps, let’s cover why this card appeals to many Australians:

- Strong rewards rate: Earn 1.5 points per $1 spent on eligible purchases — a good rate for a rewards card that doesn’t charge extremely high fees.

- Rewards flexibility: Points earned through NAB Rewards can often be transferred to a range of frequent flyer programs or redeemed for gift cards and other benefits.

- Everyday appeal: Whether it’s regular bills, groceries, fuel, or everyday purchases, you’re earning points as you spend.

This card is a particularly good fit for people who use their credit card often and can commit to paying off their balance each month — because with rewards cards, carrying a high balance can offset the benefit of the points you earn.

Step-by-Step: How to Apply for the NAB Rewards Signature Credit Card

Applying for the card is straightforward and best done through NAB’s secure online application system.

Step 1: Visit the NAB Website

Begin your journey by heading to the official NAB website and locating the Credit Cards section. From there, look for the NAB Rewards Signature Credit Card option.

If you’re already a NAB customer, logging in to your internet banking profile may help speed up the application by pre-filling some of your personal details.

Step 2: Choose Your Credit Limit

When applying, you’ll be asked to indicate the credit limit you’d like for the card. NAB will take your financial profile into account when reviewing the application and may approve a limit that is higher or lower than what you requested.

Choosing a suitable limit that reflects your spending habits and repayment ability is important because it influences your available buying power and ongoing financial management.

Step 3: Complete the Online Application Form

The application form is secure and divided into several straightforward sections:

Personal Details: This includes your full name, address, contact information, and date of birth.

Employment and Income: NAB will want information about your job, employer, annual income, and other relevant financial details.

Existing Debts and Expenses: It’s important to give accurate information on liabilities like loans or other cards you hold, as well as a realistic picture of monthly living expenses.

This part of the application helps NAB ensure that you are applying for a card that suits your financial situation and that you can manage repayments responsibly.

Step 4: Review Costs and Confirm Consent

Before you submit, NAB will present a summary of the key costs and terms associated with the card, including the ongoing annual fee, interest rates, and potential rewards terms.

You’ll also grant permission for NAB to conduct a credit check with credit reporting agencies as part of their assessment.

Step 5: Submit Your Application and Provide Verification (If Needed)

After reviewing everything, submit your application through the secure platform.

In some cases, NAB may ask for supporting documents, such as:

- Recent payslips

- Bank statements

- Proof of address

These documents can be uploaded directly through the online portal. Providing them quickly can help speed up the approval process.

Once everything is submitted, NAB will assess your application and notify you of the outcome. If approved, they’ll send your card to your Australian mailing address.

Step 6: Activate and Manage Your Card

When your card arrives, you’ll need to activate it — usually through the NAB app, internet banking, or by phone.

From there, you can begin using it for purchases and start earning points. The NAB digital tools also let you track your rewards balance, view transactions, set up automatic repayments, and manage account notifications.

Key Features of the NAB Rewards Signature Credit Card

1. Earn 1.5 Points per $1 Spent

With eligible purchases, you earn 1.5 reward points for every $1 you spend. This is a solid return compared to many basic reward cards and is particularly valuable if you’re consistent in paying off your balance.

2. Rewards Flexibility

The points you earn can often be:

- Transferred to frequent flyer programs,

- Redeemed for gift cards and merchandise,

- Used for experiences or statement credits (depending on offers available at the time).

This range of redemption options makes the card more versatile.

3. Everyday Purchase Potential

Whether you’re buying groceries, filling up at the petrol station, paying bills, or shopping online, this card earns points across a wide range of everyday spending categories.

4. Digital Tools for Tracking and Management

NAB’s app and online banking tools let you:

- Monitor your points balance,

- Track spending categories,

- Set up notifications for payments and helps with planning repayments responsibly.

Comparing the NAB Rewards Signature with the American Express Velocity Card

It’s helpful to understand how the NAB Rewards Signature Credit Card stacks up against other popular reward cards — especially something well-known like the American Express Velocity Credit Card.

While both are rewards cards, they differ in points structure, perks, fees, and how rewards are earned.

Rewards Earning Rate

- NAB Rewards Signature: Earns 1.5 points per $1 spent on eligible purchases — a competitive rate for a standard rewards card with widespread acceptance.

- American Express Velocity: Typically earns a higher rate of points per dollar spent in many everyday categories, which can make it very appealing if you spend heavily on the categories where bonus points apply.

Rewards Program Focus

- NAB Rewards Signature: Offers flexibility with partner frequent flyer programs and merchandise redemption. The points system is designed to be simple and straightforward.

- American Express Velocity: Is deeply connected to the Velocity Frequent Flyer program, meaning points can be especially valuable if you regularly fly with the linked airline partners. You may also benefit from bonus point offers for specific spend thresholds or categories.

Acceptance and Merchant Reach

One practical consideration is how widely accepted the card is at everyday merchants.

- NAB (Mastercard or Visa): These networks are accepted almost everywhere in Australia and internationally.

- American Express: While very popular, some merchants may only offer limited acceptance or charge a surcharge due to higher transaction fees — something to keep in mind if you shop at smaller stores.

Fees

Both cards have annual fees, but the structure and value you receive can differ:

- The NAB Rewards Signature annual fee may be moderately priced relative to the points you can earn.

- The American Express Velocity card often comes with a higher annual fee — but this can be balanced by more generous points and travel-related perks.

If you’re a frequent traveller or want additional travel benefits, the Velocity card’s features may justify the higher fee.

NAB Bank

Perks and Extras

- NAB Rewards Signature: Offers solid everyday rewards and flexible redemption options. It’s straightforward and transparent, making it easy to understand how points are accumulated and used.

- American Express Velocity: Often includes additional travel perks such as lounge access, travel credits, companion offers, and bonus points for reaching spend thresholds — benefits that appeal to travellers and lifestyle-focused users.

Who Each Card Suits Best

- NAB Rewards Signature: Best for everyday spenders who want a strong baseline rewards rate, broad acceptance, and flexible redemption without overly complex requirements. It’s a good fit for people who use their card regularly for normal purchases and pay off their balance each month.

- American Express Velocity: Best for people who travel frequently, want airline benefits, and are comfortable using a card with slightly higher fees in exchange for bonus perks and strong points earning potential.

Is the NAB Rewards Signature Credit Card Right for You?

The NAB Rewards Signature Credit Card is a solid choice for Australians who want to earn valuable points on everyday spending without being locked into complicated reward systems or overly high fees.

The 1.5 points per $1 earned on eligible purchases gives you a steady and meaningful way to accumulate rewards, especially if you use your card frequently and manage repayments responsibly.

Compared to high-end airline cards like the American Express Velocity Credit Card, the NAB Rewards Signature can be more accessible and easier to use for day-to-day life — especially if broad merchant acceptance and simple rewards earning are priorities.

Ultimately, the best card for you depends on how you spend, what kinds of rewards you value, and how you plan to use your points over time.

If you want this rewritten in a more promotional style, or tailored to a specific audience (like frequent travellers or everyday spenders), I can help with that too!

NAB Rewards Signature: Key Features and Eligibility

The NAB Rewards Signature card lets you collect rewards for everyday spending. You can swap points for travel, gift cards, goods, or cash off your statement. This guide covers what the NAB Rewards program offers, key features of the Signature card, and what to know about eligibility and costs.

Overview of the NAB Rewards Signature program

Spending on eligible items earns points, added to your account usually monthly. The rewards portal and NAB’s online banking let you check points, see deals, and use points. Always read the fine print for details on when points expire and transferring points rules before you decide.

Eligibility criteria for Australian applicants

You need to follow NAB’s rules, be 18 or older, and live in Australia or be a citizen to apply. NAB will look at your income, job, and if you can afford the card. Your credit score is important too; past money troubles might stop approval.

To apply, show ID and how much you earn, like a payslip or tax info. If you’re already with NAB and in good standing, getting the card might be easier.

Card benefits: points earning rates and welcome offers

You usually earn points for buying things, more for special categories. But, not everything earns points, like cash advances or paying government fees.

Intro deals often need you to spend a certain amount quickly to get extra points. Make sure you know the spending target and what buys count so you can get those points.

Ongoing fees, interest rates and balance transfer details

The card has an annual fee that might be free at first. Think about these fees when figuring out if the rewards are worth it. Fees for late payment or using your card overseas can also cut into your rewards.

The interest rate for buying things can change, and paying off your monthly bill avoids interest. Getting cash costs more in interest. If there’s a deal to move a balance to this card, it might start with low interest which then goes up. Always check the full details on fees and the rate after the deal ends.

How to Apply and Practical Tips to Maximise Points

Before you start, check what documents you need and understand the welcome offer. A quick checklist can make the process easier and help you dodge common mistakes. Gather your identity documents, recent payslips, or an ATO Notice of Assessment. You’ll also need proof of address, like a utility bill, and any credit application documents required in Australia. Decide whether to apply for a NAB card online, use NAB Internet Banking if you’re already a customer, or visit a branch.

Step-by-step application process for Australian residents

- Fill in your personal details, income, and expenses carefully when learning how to apply for a NAB Rewards Signature.

- Follow the steps of the NAB Signature application: choose card options, disclose existing debts, and agree to a credit check.

- Upload needed documents if asked for NAB ID verification and proof of income.

- Be ready for quick decisions or short wait times; stay updated via your email or NAB messages for any extra steps.

Verification documents and common application pitfalls

- For the 100-point ID check, NAB commonly accepts an Australian driver licence, passport, Medicare card, or proof of age card.

- Use recent payslips, PAYG summaries, or tax returns for income proof; Centrelink statements work too, if applicable.

- Avoid usual mistakes like mismatched names or addresses, not stating all expenses, not declaring all debts, or missing documents.

- Avoid applying for multiple cards in a short time to protect your credit score and speed up approval.

Post-approval and switching or upgrading

- Once approved, agree to the contract, choose a PIN, and activate the card. Link it to your NAB Rewards account and sign up on the rewards portal.

- Use card controls and alerts to secure your account and keep track of points.

- If you’re already a NAB customer, you can ask for an upgrade or switch products through NAB Internet Banking or ask a banker about credit limits and points.

Smart spending strategies to boost points accrual

- Focus your spending on areas like groceries, fuel, and subscriptions to earn more points. Plan your spending to earn big on everyday categories.

- Meet welcome offer targets smartly by timing big buys during the qualifying period.

- Avoid interest by paying your balance in full each month to protect the value of your rewards and boost your NAB points.

- Use regular payments for a steady flow of points. Check the fine print for any spending categories that don’t earn points.

- Consider adding an authorised user to combine spending, but remember the main cardholder is responsible for the account.

Partner offers, bonus categories and seasonal promotions

- Keep an eye on NAB’s partner airlines, hotels, retailers, and gift card offers. These partnerships and their benefits can change, so review the rewards site regularly.

- Watch for NAB’s extra points offers and special credit card deals around sales events like EOFY, Black Friday or Boxing Day. Using these promotions wisely can supercharge your NAB Rewards.

- Sign up for NAB emails and opt into promotional messages. Also, link your card to merchant offers when you need to activate them before buying.

Redeeming points: best value options and transfer partners

- You can use points for flights, hotel stays, goods, gift cards, cashbacks, and frequent flyer program transfers.

- Transferring points to partner programs or using them for travel usually offers the most value, stretching your points further for flights and upgrades.

- Before transferring, check the conversion rates, fees, and minimums. Remember to consider taxes, extra charges, and blackout dates when you use your points.

- If you can pool points with family or transfer them, do it to access better rewards. Book early and look at mixed payment options to best use points.

Conclusion

The NAB Rewards Signature card is a solid option for Aussies who avoid carrying a balance. It’s great for those who funnel their spending through the card and use the welcome offers. However, there’s an annual fee and normal interest rates to consider if you don’t pay off your balance each month.

Thinking about the NAB Rewards Signature card? Consider the annual fee and interest rates against potential points. Make sure you’re eligible and have all your documents ready, like ID and proof of income. Aim to use welcome offers wisely to avoid extra debt.

Whether the NAB Rewards Signature card is right for you depends on your spending habits. Check out the latest details on NAB’s website. Sign up for the rewards program, and watch out for special deals. Remember to set up auto-pay to dodge interest charges and keep an eye on your points to maximize rewards.

Ready to make a decision? Compare the NAB Rewards Signature card with others from NAB and different banks. Use NAB’s tools for personalized offers. Apply online or visit a NAB branch when you feel it’s the right fit for your budget and lifestyle goals.

Conteúdo criado com auxílio de Inteligência Artificial